Cost & Management accounting

Question 1

Distinguish between Cost control and Cost reduction

Answer

Cost Control and Cost Reduction:

Cost control is operated through setting standards or targets and comparing actual performance therewith, with a view to identify deviation from standards or norms and taking corrective action in order to ensure that future performance conforms to standards or norms.

Cost reduction is a continuous process of critical cost examination, analysis and discharge of standards. Each subject of business viz products, process, procedures, methods, origin, personnel etc is critically examined and reviewed with a view of improving the efficiency &effectiveness and reducing the costs. Even in an organization where efficient cost control is in operation, there is always room for cost reduction.

Question 2

Discuss the essentials of a good Cost Accounting system.

Answer

Essentials of a good Cost Accounting System: The essential features, which a good Cost Accounting System should possess, are as follows:

-

Informative and Simple: Cost Accounting System should be tailor-made, practical,simple and capable of meeting the requirements of a business concern.

-

Accuracy: The data to be used by the Cost Accounting System should be accurate; otherwise it may distort the output of the system.

-

Support from Management: Necessary cooperation and participation of executives from various departments of the concern is essential for developing a good system of Cost Accounting.

-

Cost- Benefit: The Cost of installing and operating the system should justify the results.

-

Precise Information: The system of costing should not sacrifice the utility by introducingmeticulous and unnecessary details.

-

Procedure: A carefully phased programme should be prepared by using network analysisfor the introduction of the system.

-

Trust: Management should have faith in the Costing System and should also provide a helping hand for its development and success.

Question 3

Discuss cost classification based on variability and controllability.

Answer

Cost classification based on variability

Fixed cost – these are costs, which do not change in total despite changes of a cost driver. A fixed cost is fixed only in relation to a given relevant range of the cost driver and a given time span. Rent, insurance, depreciation of factory building and equipment are examples of fixed costs where the final product produced is the cost object.

Variable costs- these are costs which change in total in proportion to changes of cost driver.

Direct material, direct labour are examples of variable costs in cases where the final product produced is the cost object.

Semi-variable costs – These are partly fixed and partly variable in relation to output e.g. telephone and electricity bill.

Cost classification based on controllability

Controllable costs – are incurred in a particular responsibility center and relate to a defined time span. They can be influenced by the action of the executive heading the responsibility center e.g. direct costs.

Uncontrollable costs – are costs which are not influenced by the action of the responsibility manager e.g. expenditure incurred by the tool room is controllable by the foreman in charge ofthat section, but the share of tool room expenditure which is apportioned to the machine shop is not controllable by machine shop foreman.

Question 4

Distinguish between

-

Profit Centres and Investment Centres.

-

Product Cost and Period Cost.

Answer

-

Profit Centres and investment centres

A profit centre is a centre where the manager has the responsibility of generating and maximising profits. In such centres, the manager is responsible for revenue and cost. Investment centres are those centres which are concerned with earning an adequate ROI. In such centres, the manager is responsible for investment, revenue and cost.

2. Product costs and period costs

Product costs are costs which are associated with purchase and sale of goods. These are costs are used for inventory valuation and incurred up to factory stage.

Period costs are costs, which are not assigned to the products but are charged as expenses against revenues of the period in which they are incurred e.g. Selling, General Administrative and Distribution overheads.

Question 5

Explain controllable and non-controllable cost with examples.

Answer

Controllable costs are those which can be influenced by the action of a specified member of an undertaking. A business organization is usually divided into a number of responsibility centres and each such centre is headed by an executive. Controllable costs incurred in a particular responsibility centre can be influenced by the action of the executive heading that responsibility centre. Direct costs comprising direct labour, direct materials, direct expenses and some of the overhead are generally controllable by the shop level management.

Non-controllable costs are those which cannot be influenced by the action of a specified member of an undertaking. For example, expenditure incurred by the tool room is controllable by the tool room manager but the share of the tool room expense which is apportioned to the machine shop cannot be controlled by the machine shop manager. It is only in relation to a particular individual that a cost may be specified as controllable or not.

Note:

1. A supervisor may be unable to control the amount of managerial remuneration allocated to his department but for the top management this would be a controllable cost.

2. Depreciation would be a non-controllable cost in the short-term but controllable in the long terms.

Question 6

Distinguish between cost control and cost reduction.

Answer

Difference between Cost Control and Cost Reduction

|

Cost Control |

Cost Reduction |

|

1. Cost control aims at maintaining the costs in accordance with the established standards. |

1. Cost reduction is concerned with reducing costs. It challenges all standards and endeavors to better them continuously |

|

2. Cost control seeks to attain lowest possible cost under existing conditions. |

2. Cost reduction recognises no condition as permanent, since a change will result in lower cost. |

|

3. In case of Cost Control, emphasis ison past and present |

3.In case of cost reduction it is on present and future. |

|

4.Cost Control is a preventive function |

4.Cost reduction is a corrective function. It operates even when an efficient cost control system exists. |

|

5. Cost control ends when targets are achieved |

5.Cost reduction has no visible end. |

Question-7

STATE the Cost Control and Cost Reduction objectives of Cost and Management Accounting system.

Answer:

Among other objectives of cost and management accounting system, cost control and cost reduction are principal objectives. Cost control objective ensures the compliance with the set standard of procedures, Cost Reduction objective explores the possibilities of improvements in terms of both quantitative and qualitative aspects. Both objectives are briefly explained as below:

Cost Control: Maintaining discipline in expenditure is one of the main objectives of a good cost and management accounting system. It ensures that expenditures are in consonance with predetermined set standard and any variation from these set standards is noted and reported on continuous basis. To exercise control over cost, following steps are followed:

-

Determination of pre-determined standard or results: Standard cost or performance targets for a cost object or a cost centre is set before initiation of production or service activity. These are desired cost or result that need to be achieved.

-

Measurement of actual performance: Actual cost or result of the cost object or cost centre is measured. Performance should be measured in the same manner in which the targets are set i.e. if the targets are set up operation-wise, and then the actual costs should also be collected and measured operation-wise to have a common basis for comparison.

-

Comparison of actual performance with set standard or target: The actual performance so measured is compared against the set standard and desired target. Any deviation(variance) between the two is noted and reported to the appropriate person or authority.

-

Analysis of variance and action: The variance in results so noted are further analysed to know the reasons for variance and appropriate action is taken to ensure compliance in future. If necessary, the standards are further amended to take developments into account.

Cost Reduction: It may be defined "as the achievement of real and permanent reduction in the unit cost of goods manufactured or services rendered without impairing their suitability for the use intended or diminution in the quality of the product."

Cost reduction is an approach of management where cost of an object is believed to be further reduced. No cost is termed as lowest and every possibility of cost reduction is explored. To do cost reduction, the following action is taken:

-

Each activity within an entity is segmented to analyse and identify value added and non value added activities. All non-value added activities are eliminated without affecting the essential characteristics of the product or process. Value chain Analysis, a strategic tool, developed by Michael Porter, is one of the methods to do value analysis.

-

Conducting continuous research and study to know better way to do anything.

The three-fold assumptions involved in the definition of cost reduction may be summarised asunder:

-

There is a saving in unit cost.

-

Such saving is of permanent nature.

-

The utility and quality of the goods and services remain unaffected, if not improved.

Question-8

STATE in brief how Cost Accounting and Management Accounting is related or different from each other.

Answer:

The term Cost Accounting and Management Accounting is interchangeably by various laureates as both the disciplines are interrelated. Management accounting to enable its users to take timely and judicious decisions takes inputs from cost accounting, financial accounting, statistics and operation management tools etc. Among other sources of information Cost Accounting system provides cost related information. There are few differences between these two disciplines which are tabulated as below:

Difference between Cost Accounting and Management Accounting

|

|

Basis |

Cost Accounting |

Management Accounting |

|

(i) |

Nature |

It records the quantitative aspect only. |

It records both qualitative and quantitative aspect. |

|

(ii) |

Objective |

It records the cost of producing a product and providing a service. |

It Provides information to management for planning and co-ordination. |

|

(iii) |

Area |

It only deals with cost Ascertainment. |

It is wider in scope as it includes financial accounting, budgeting, taxation, planning etc. |

|

(iv) |

Recording of data |

It uses both past and present figures. |

It is focused with the projection of figures for future. |

|

(v) |

Development |

Its development is related to industrial revolution. |

It develops in accordance to the need of modern business world. |

|

(vi) |

Rules and Regulation |

It follows certain principles and procedures for recording costs of different products. |

It does not follow any specific rules and regulations. |

Question 9

IPL Limited uses a small casting in one of its finished products. The castings are purchased from a foundry. IPL Limited purchases 54,000 castings per year at a cost of Rs800 per casting.

The castings are used evenly throughout the year in the production process on a 360- day-per- year basis. The company estimates that it costs Rs9,000 to place a single purchase order and about Rs300 to carry one casting in inventory for a year. The high carrying costs result from the need to keep the castings in carefully controlled temperature and humidity conditions, and from the high cost ofinsurance.

Delivery from the foundry generally takes 6 days, but it can take as much as 10days. The daysofdeliverytimeandpercentageoftheiroccurrenceareshowninthefollowingtabulation:

|

Delivery time (days): |

6 |

7 |

8 |

9 |

10 |

|

Percentage of occurrence: |

75 |

10 |

5 |

5 |

5 |

Required:

-

Compute the economic order quantity(EOQ).

-

Assume the company is willing to assume a 15% risk of being out of stock. What would be the safety stock? The re-order point?

-

Assume the company is willing to assume a 5% risk of being out of stock. What would be the safety stock? The re-order point?

-

Assume 5% stock-out risk. What would be the total cost of ordering and carrying inventory for one year?

-

Refer to the original data. Assume that using process re-engineering the company reduce sits cost of placing a purchase order to only Rs600. In addition, company estimates that when the waste and inefficiency caused by inventories are considered, the true cost of carrying a unit in stock is Rs720 per year.

-

Compute the new EOQ.

How frequently would the company be placing an order, as compared to the old purchasing policy?

Answer

-

Computation of economic order quantity (EOQ):

|

(A) |

Annual requirement |

= |

54,000 castings |

|

(C) |

Cost per casting |

= |

Rs800 |

|

(O) |

Ordering cost |

= |

Rs9,000 / order |

(c i)Carrying cost per casting p.a. = Rs300

\(E O Q=\sqrt{\frac{2 A O}{C \times i}}=\sqrt{\frac{2 \times 54000 \times 9000}{300}}=1800 \text { castings }\)

2) Safety stock

(Assuming a 15% risk of being out of stock)

Safety stock for one day = 54,000/360 days = 150 castings

Re-order point = Minimum stock level + Average lead time X Average consumption

= 150 + 6 x 150 = 1,050 castings

3) Safety stocks:

(Assuming a 5% risk of being out of stock)

Safety stock for three days = 150 x 3 days = 450 castings

Re-order point = 450 castings + 900 castings = 1,350 castings

4) Total cost of ordering = (54,000/1,800) x Rs 9,000 = Rs 2,70,000

Total cost of carrying = (450 + ½ x 1,800) Rs 300 = Rs 4,05,000

b)Total number of orders to be placed in a year are180. Each order is to be placed after 2 days (1 year = 360 days). Under old purchasing policy each order is placed after 12 days.

Question 10

Discuss ABC analysis as a system of Inventory control.

Answer

ABC Analysis as a system of inventory control

It exercises discriminating control over different items of stores classified on the basis of investment involved.

‘A’ category of items consists of only a small %age i.e. approximately 10% of total items handled by stores but requires heavy investment, about 70% of inventory value, because of their high prices or heavy requirement or both.

‘B’ category of items are relatively less important. They may be approximately 20% of the total items of materials handled by stores. The %age of investment required is approximately 20% of total investment in inventories.

‘C’ category of items do not require much investment. It may be about 10% of total inventory value but they are nearly 70% of the total items handled by store. EOQ, re-order level concepts are usually used in case of ‘A’ category items.

Question 11

SK Enterprise manufactures a special product “ZE”. The following particulars were collected for the year 2004:

Annual consumption 12,000 units (360 days) Cost per unit Rs1

Ordering cost Rs12 per order Inventory carrying cost 24% Normal lead time 15 days

Safety stock 30 days consumption

Required:

-

Re-order quantity

-

Re-order level

-

What should be the inventory level (ideally) immediately before the material order is received?

Answer

(i) How much should be ordered each time i.e., Economic Order Quantity (EOQ)

Question 12

Discuss the treatment of spoilage and defectives in cost accounting

Answer

Normal spoilage (which is inherent in the operation) costs are included in costs either by charging the loss due to spoilage to the production order or charging it to production overhead so that it is spread over all the products. Any value realized from the sale of spoilage is credited to production order or production overhead accounts, as the case may be. The cost of abnormal spoilage is charged to Costing P/L A/C. When spoiled work is the result of rigid specification, the cost of spoiled work is absorbed by good production while the cost ofdisposal is charged to production overhead.

Defectives that are considered inherent in the process and are identified as normal can be recovered by using the following method.

-

Charged to goods products

-

Charged to general overheads

-

Charged to departmental overheads

If defectives are abnormal, they are charged to Costing Profit and Loss Account.

Question 13

PQR Limited produces a product which has a monthly demand of 52,000 units. The product requires a component X which is purchased at Rs15 per unit. For every finished product, 2 units of Component X are required. The Ordering cost is Rs350 per order and the Carrying cost is 12% p.a.

Required:

-

Calculate the economic order quantity for Component X.

-

If the minimum lot size to be supplied is 52,000 units, what is the extra cost, the company has to incur?

-

What is the minimum carrying cost, the Company has to incur?

Answer

Demand of ‘X’ is 1,04,000 units (2 × 52,000 units) as per instruction that for every finished product , 2 units of component ‘X’ are required.

Question 14

PQR Ltd., manufactures a special product, which requires ‘ZED’. The following particulars were collected for the year 2005-06:

(i) Monthly demand of Zed : 7,500 units

(ii) Cost of placing an order :Rs500

(iii)Re-order period : 5 to 8 weeks

(iv) Cost per unit :Rs60

(v)Carrying cost % p.a. : 10%

(vi)Normal usage : 500 units per week

(vii) Minimum usage : 250 units per week

(viii) Maximum usage : 750 units per week

Required:

(i) Re-order quantity.

(ii) Re-order level.

(iii) Minimum stock level.

(iv) Maximum stock level.

(v) Average stock level.

Answer

(iv) Maximum stock level

= Re-order level + Re-order quantity – (Minimum usage Minimum re-order period)

= 6,000 + 3,873 – (5×250)

= 8,623 units

(v) Average stock level

= ½ (Minimum stock level + Maximum stock level)

= ½ (2,750 + 8,623)

= 5,687 units

Question 15

Discuss the use of perpetual inventory records and continuous stock verification, and its advantages.

Answer

Use of perpetual inventory records and continuous stock verification: Perpetual inventory represents a system of records maintained by the stores department. These are Bin cards and Stores ledger.

Bin Card is a quantitative record of receipt, issue and closing balance of each item of stores. Separate bin cards are maintained for each item. Each card is filled up with physical movement of goods i.e. on receipt and issue.

Stores Ledger is quantitative and value record of receipt, issue and closing balance of eachitem of stores. It is filled with the help of goods received note and material issue requisitions.

A perpetual inventory is usually checked by a programme of continuous stock taking. Continuous stock taking means physical checking of those records with actual stock.

Advantages of perpetual inventory

-

Physical stocks can be counted and book balances adjusted as and when desired without waiting for entire stock taking to be done.

-

Quick compilation of Profit and Loss Account due to prompt availability of stock figures.

-

Discrepancies are easily located and thus corrective action can be promptly taken.

-

A systematic review of the perpetual inventory reveals the existence of surplus, dormant, obsolete and slow moving materials, so that remedial measures may be taken in time.

-

Fixation of various stock levels and checking of actual balance in hand.

Question 16

ZED Company supplies plastic crockery to fast food restaurants in metropolitan city. One of its products is a special bowl, disposable after initial use, for serving soups to its customers. Bowls are sold in pack 10 pieces at a price of Rs50 per pack.

The demand for plastic bowl has been forecasted at a fairly steady rate of 40,000 packs every year. The company purchases the bowl direct from manufacturer at Rs40 per pack within a three days lead time. The ordering and related cost is Rs8 per order. The storage cost is 10% per cent per annum of average inventory investment.

Required:

(i) Calculate Economic Order Quantity.

(ii) Calculate number of orders needed every year.

(iii) Calculate the total cost of ordering and storage bowls for the year.

(iv) Determine when should the next order to be placed. (Assuming that the company does maintain a safety stock and that the present inventory level is 333 packs with a year of 360 working days.)

Answer

333 / 400 x 3.6 days 3 days requirement

(c) Time interval for placing next order

Inventory left for day’s requirement – Lead time of delivery 3 day’s requirements – 3 days lead time = 0

This means that next order for the replenishment of supplies has to be placed immediately.

Question 17

ABC Limited has received an offer of quantity discounts on its order of materials as under:

Price per tonnes Tonnes (Rs) Nos.

4,800 Less than 50

4,680 50 and less than 100

4,560 100 and less than 200

4,440 200 and less than 300

4,320 300 and above

The annual requirement for the material is 500 tonnes. The ordering cost per order is Rs6,250 and the stock holding cost is estimated at 25% of the material cost per annum.

Required :

(i) Compute the most economical purchase level

(ii) Compute E.O.Q. if there are no quantity discounts and the price per tonne is Rs5,250.

Answer

-

Calculation of most economical purchase level:

A= Annual requirement = 500 tonnes

The total cost of purchase ordering cost and carrying cost of 500 tonnes is minimum Rs 23,32,437.50 when the order size is 300 tonnes. Hence most economical purchase level is 300 tonnes.

= 69 tonnes

A is the annual requirement for the material. O is the ordering Cost per order

Ci is the carrying Cost per unit per annum.

Question 19

Distinguish between bill of material and material requisition note.

Answer

|

Bills of material |

Material Requisition Note |

|

1. It is document by the drawing office |

1.It is prepared by the foreman of the consuming department. |

|

2. It is a complete schedule of component parts and raw materials required for a particular job or work order. |

2. It is a document authorizing Store- Keeper to issue Material to the consuming department. |

|

3. It often serves the purpose of a Store Requisition as it shown the complete schedule of materials required for a particular job i.e. it can replace stores requisition. |

3. It cannot replace a bill of material. |

|

4. It can be used for the purpose of quotation |

4. It is useful in arriving historical cost only. |

|

5. It helps in keeping a quantitative control on materials draw through stores Requisition. |

5. It shows the material actually drawn from stores. |

Question 20

Following details are related to a manufacturing concern:

|

Re-order Level |

1,60,000 units |

|

Economic Order Quantity |

90,000 units |

|

Minimum Stock Level |

1,00,000 units |

|

Maximum Stock Level |

1,90,000 units |

|

Average Lead Time |

6 days |

|

Difference between minimum lead time and Maximum lead time |

4 days |

Calculate:

(i) Maximum consumption per day Minimum consumption per day

Answer

Difference between Minimum lead time Maximum lead time = 4 days Max. lead time – Min. lead time = 4 days

Or, Max. lead time = Min. lead time + 4 days............................................ (i)

Average lead time is given as 6 days i.e.

Max. Lead time Min. Lead time / 2 = 6 days......................................................................................................................... (ii)

Putting the value of (i) in (ii),

Min. lead time + 4 days Min. Lead time / 2 = 6 days

Or, Min. lead time + 4 days + Min. lead time = 12 days Or, 2 Min. lead time = 8 days

Or, Minimum lead time = 8days / 2 = 4 days

Putting this Minimum lead time value in (i), we get Maximum lead time = 4 days + 4 days = 8 days

(i) Maximum consumption per day:

Re-order level = Max. Re-order period × Maximum Consumption per day 1,60,000 units = 8 days × Maximum Consumption per day

Or, Maximum Consumption per day = 1,60,000units / 8days = 20,000 units

(ii) Minimum Consumption per day:

Maximum Stock Level =

Re-order level + Re-order Quantity – (Min. lead time × Min. Consumption per day)

Or, 1,90,000 units = 1,60,000 units + 90,000 units – (4 days × Min. Consumption per day) Or, 4 days × Min. Consumption per day = 2,50,000 units – 1,90,000 units

Or, Minimum Consumption per day = 60,000 units / 4 days = 15,000 units

Question 21

A company manufactures 5,00,000 units of a product per month. The cost of placing an order is Rs1,000. The purchase price of the raw material is Rs50 per kg. The re-order period is 4 to 8 days. The consumption of raw materials varies from 14,000 kg to 18,000 kg per day, the average consumption being 16,000 kg. The carrying cost of inventory is 20% per annum.

You are required to CALCULATE

(i) Re-order quantity

(ii) Re-order level

(iii) Maximum level

(iv) Minimum level

(v) Average stock level

Answer:

(i)Reorder Quantity (ROQ) = 34,176 kg. (Refer to working note)

(ii) Reorder level (ROL) = Maximum usage × Maximum re-order period

= 18,000 kg. × 8 days = 1,44,000 kg.

(iii) Maximum level = ROL + ROQ – (Min. usage × Min. re-order period)

= 1,44,000 kg. + 34,176 kg. – (14,000 kg.× 4 days)

= 1,22,176 kg.

(iv) Minimum level = ROL – (Normal usage × Normal re-order period)

= 1,44,000 kg. – (16,000 kg. × 6 days)

= 48,000 kg.

Question 22

ZED Limited is working by employing 50 skilled workers. It is considered the introduction of incentive scheme-either Halsey scheme (with 50% bonus) or Rowan scheme of wage payment for increasing the labour productivity to cope up the increasing demand for the product by 40%. It is believed that proposed incentive scheme could bring about an average 20% increase over the present earnings of the workers; it could act as sufficient incentive for them to produce more.

Because of assurance, the increase in productivity has been observed as revealed by the figures for the month of April, 2004.

Hourly rate of wages (guaranteed) = Rs 30

Average time for producing one unit by one worker at the previous performance (This may be taken as time allowed) = 1.975 hours

Number of working days in the month = 24

Number of working hours per day of each worker = 8

Actual production during the month = 6,120 units

Required:

(i) Calculate the effective rate of earnings under the Halsey scheme and the Rowan scheme.

(ii) Calculate the savings to the ZED Limited in terms of direct labour cost per piece.

(iii) Advise ZED Limited about the selection of the scheme to fulfill their assurance.

Answer

Working notes:

1. Computation of time saved ( in hours) per month :

= (Standard production time of 6,120 units – Actual time taken by the workers)

= (6,120 units x 1.975 hours – 24 days x 8 hrs per day x 50 skilled workers)

= (12,087 hours – 9,600 hours)

= 2,487 hours

2. Computation of bonus for time saved hours under Halsey and Rowan schemes:

Time saved hours = 2,487 hours (Refer to working note 1)

Wage rate per hour = Rs 30

Bonus under Halsey Scheme = ½ x 2,487 hours x Rs 30 (with 50% bonus) = Rs 37,305

(i) Computation of effective rate of earnings under the Halsey and Rowan schemes:

Total earnings (under Halsey scheme) = Time wages + Bonus (Refer to working note 2)

= 24 days x 8 hours x 50 skilled workers x Rs 30 + Rs 37,305

= Rs 2,88,000 + Rs 37,305 = Rs 3,25,305

Total earnings (under Rowan scheme) = Time wages + Bonus (Refer to working note 2)

= Rs 2,88,000 + Rs 59,258.38

= Rs 3,47,258.38

Effective rate of earnings per hour (under Halsey Plan Rs 33.89 (Rs 3,25,305 ÷ 9,600 hrs.)

Effective rate of earnings per hour (under Rowan Plan Rs 36.17 (Rs 3,47,258.38 ÷ 9,600 hrs)

(ii) Savings to the ZED Ltd. in terms of direct labour cost per piece:

Rs

Direct labour cost (per unit) under time wages system = 59.25 (1.975 times per unit × Rs 30)

Direct labour cost (per unit) under Halsey Plan = 53.15 (Rs 3,25,305 ÷ 6,120 units)

Direct labour cost (per unit) under Rowan Plan = 56.74 (Rs 3,47,258.38 ÷ 6,120 units)

Savings of direct labour cost under:

Halsey Plan= Rs 6.10 (Rs 59.25 - 53.15)

Rowan Plan = Rs 2.51 (Rs 59.25 56.74)

(iii) Advise to ZED Ltd : (about the selection of the scheme to fulfill assurance)

Halsey scheme brings more savings to the management of ZED Ltd, over the present earnings of Rs 2,88,000 but the other scheme viz Rowan fulfils the promise of 20% increase over the present earnings of Rs 2,88,000 by paying 20.58% in the form of bonus. Hence Rowan Plan may be adopted.

Question 23

Discuss the Gantt task and bonus system as a system of wage payment and incentives.

Answer

Gantt Task and Bonus System

This system is a combination of time and piecework system. According to this system a high standard or task is set and payment is made at time rate to a worker for production below the set standard.

Wages payable to workers under the plan are calculated as under:

|

Output |

Payment |

|

(i) Output below standard |

Guaranteed time rate |

|

(ii) Output at standard |

Time rate plus bonus of 20% (usually) of time rate |

|

(iii) Output over standard |

High piece rate on worker’s output .(It is so fixed ,so as to include a bonus of 20% of time rate) |

Question 24

The existing Incentive system of Alpha Limited is as under:

Normal working week 5 days of 8 hours each plus 3 late shifts of 3 hours each

Rate of Payment Day work: Rs160 per hour

Late shift: Rs225 per hour

Average output per operator for 49-hours week i.e. 120 articles including 3 late shifts

In order to increase output and eliminate overtime, it was decided to switch on to a system of payment by results. The following Information is obtained:

Time-rate (as usual) :Rs160 per hour

Basic time allowed for 15 articles : 5 hours Piece-work rate : Add 20% to basic piece-rate Premium Bonus : Add 50% to time.

Required:

Prepare a Statement showing hours worked, weekly earnings, number of articles produced and labour cost per article for one operator under the following systems:

a) Existing time-rate

b)Straight piece-work

c) Rowan system

d)Halsey premium system

Assume that 135 articles are produced in a 40-hour week under straight piece work, Rowan Premium system, and Halsey premium system above and worker earns half the time saved under Halsey premium system.

Answer

Table showing Labour Cost per Article

|

Method of Payment |

Hours worked |

Weekly earnings |

Number articles produced |

labour cost per article |

|

|

Existing time rate |

49 |

Rs 8,425.00 |

120 |

Rs 70.21 |

|

|

Straight piece rate system |

40 |

Rs 8,640.00 |

135 |

Rs 64.00 |

|

|

Rowan Premium System |

40 |

Rs 9,007.41 |

135 |

Rs 66.72 |

|

|

Halsey Premium System |

40 |

Rs 8,600.00 |

135 |

Rs 63.70 |

|

Time allowed for 135 articles = 67.5 hours

Actual time taken for 135 articles = 40 hours

Question 25

Discuss the treatment of Idle time and Overtime premium in Cost Accounting.

Answer

Treatment of Idle time and Overtime Premium in Cost Accounting

-

Normal idle time is treated as a part of the cost of production. Thus, in the case of direct workers, an allowance for normal idle time is built into labour cost rates. In case of indirect workers, normal idle time is spread over all the products or jobs through the process of absorption of factory overheads.

-

Abnormal idle time cost is not included as a part of production cost and is shown as a separate item in costing Profit and Loss Account.

-

Management should aim at eliminating controllable idle time and on a long-term basis reduce even the normal idle time.

-

If overtime is resorted to at the desire of the customer, then overtime premium may b charged to the job directly.

-

If overtime is required to cope with general production programme or for meeting urgent orders, the overtime premium should be treated as overhead cost of the particular department/cost centre.

Question 26

Enumerate the remedial steps to be taken to minimize the labour turnover.

Answer

The following steps are useful for minimizing labour turnover:

-

Exit interview: An interview be arranged with each outgoing employee to ascertain the reasons of his leaving the organization.

-

Job analysis and evaluation: to ascertain the requirement of each job.

-

Organisation should make use of a scientific system of recruitment, placement and promotion for employees.

-

Organisation should create healthy atmosphere, providing education, medical and housing facilities for workers.

-

Committee for settling workers grievances.

Question 27

Distinguish between Job evaluation and Merit rating.

Answer

Job Evaluation and Merit Rating:

-

Job evaluation is the assessment of the relative worth of jobs within a company and merits rating are the assessment of the relative worth of the man behind the job.

-

Job evaluation and its accomplishment are means to set up a rational wage and salary structure where as merits rating provides a scientific basis for determining fair wages for each worker based on his ability and performance.

-

Job evaluation simplifies wage administration by bringing an uniformity in wage rates where as merits rating is used to determine fair rate of pay for different workers.

Question 28

Standard Time for a job is 90 hours. The hourly rate of guaranteed wages is Rs50. Because of the saving in time a worker a gets an effective hourly rate of wages of Rs60 under Rowan premium bonus system. For the same saving in time, calculate the hourly rate of wages a worker B will get under Halsey premium bonus system assuring 40% to worker.

Answer

Increase in Hourly Rate of Wages (Rowan Plan) is (Rs 60 – Rs 50) = Rs 10

This is Equal to

Question 29

Which is better plan out of Halsey 50 percent bonus scheme and Rowan bonus scheme for an efficient worker? In which situation the worker get same bonus in both schemes?

Answer

Rowan Bonus Scheme pays more bonus if the time saved is below the 50 per cent of time allowed and if the time saved is more than 50 percent of time allowed then Halsey bonus scheme pays more bonus. Generally, time saved by a worker is not more than 50 per cent of time allowed. So, the Rowan bonus scheme is better for an efficient worker. When the time saved is equal to 50 per cent of time allowed then both plans pays same bonus to a worker.

Question 30

Enumerate the causes of labour turnover.

Answer

Causes of Labour Turnover : The main causes of labour turnover in an organisation/ industry can be broadly classified under the following three heads :

a) Personal Causes;

b) Unavoidable Causes; and

c)Avoidable Causes.

Personal causes are those which induce or compel workers to leave their jobs; such causes include the following:

-

Change of jobs for betterment.

-

Premature retirement due to ill health or old age.

-

Domestic problems and family responsibilities.

-

Discontent over the jobs and working environment.

Unavoidable causes are those under which it becomes obligatory on the part of management to ask one or more of their employees to leave the organisation; such causes are summed up as listed below:

-

Seasonal nature of the business;

-

Shortage of raw material, power, slack market for the product etc.;

-

Change in the plant location;

-

Disability, making a worker unfit for work;

-

Disciplinary measures;

-

Marriage (generally in the case of women).

Avoidable causes are those which require the attention of management on a continuous basis so as to keep the labour turnover ratio as low as possible. The main causes under this case are indicated below:

-

Dissatisfaction with job, remuneration, hours of work, working conditions, etc.,

-

Strained relationship with management, supervisors or fellow workers;

-

Lack of training facilities and promotional avenues;

-

Lack of recreational and medical facilities;

-

Low wages and allowances.

Question 31

A skilled worker is paid a guaranteed wage rate of Rs120 per hour. The standard time allowed for a job is 6 hour. He took 5 hours to complete the job. He is paid wages under Rowan Incentive Plan.

(i) Calculate his effective hourly rate of earnings under Rowan Incentive Plan.

(ii) If the worker is placed under Halsey Incentive Scheme (50%) and he wants to maintain the same effective hourly rate of earnings, calculate the time in which he should complete the job.

Answer

(i) Effective hourly rate of earnings under Rowan Incentive Plan Earnings under Rowan Incentive plan =

Question 32

The following particulars have been extracted from the records of MJ Ltd.

|

|

Workers |

||

|

A |

B |

C |

|

|

Actual hours worked in a month |

152 |

160 |

136 |

|

Hourly rate of wages |

Rs50 |

Rs55 |

Rs48 |

|

Production in units |

|

|

|

|

Product- P |

84 |

- |

240 |

|

Product- Q |

144 |

- |

540 |

|

Product -R |

184 |

100 |

- |

Standard time allowed per unit of each product is:

P Q R

Minutes 12 18 30

For the purpose of piece rate,each minute is valued at Rs1/-

You are required to CALCULATE the wages of each worker under:

(i) Guaranteed hourly rate basis

(ii) Piece work earnings basis, but guaranteed at 75% of basic pay (guaranteed hourly rate)if the earnings are less than 50% of basic pay.

(iii) Premium bonus basis where the worker receives bonus based on Rowan scheme.

Answer:

-

Computation of wages of each worker under guaranteed hourly rate basis

|

Workers |

Actual hours worked in a week |

Hourly rate of wages (Rs) |

Wages (Rs) |

|

(a) |

(b) |

(c) |

(d) = (b) × (c) |

|

A

B |

152

160 |

50

55 |

7,600

8,800 |

|

C |

136 |

48 |

6528 |

-

Computation of wages of each worker under piece work earnings basis

|

|

Worker A |

Worker B |

Worker C |

||||

|

Product |

Rate per unit |

Units |

Wages (Rs) |

Units |

Wages (Rs) |

Units |

Wages (Rs) |

|

(a) |

(b) |

(c) |

(d= b*c) |

(e) |

(f = b*e) |

(g) |

(h=b*g) |

|

P

Q

R |

12

18

30 |

84

144

184 |

1,008

2,592

5,520 |

-

-

100 |

-

-

3,000 |

240

540

- |

2,880

9,720

- |

|

|

9,120 |

|

3,000 |

|

12,600 |

||

Since each worker has been guaranteed at 75% of basic pay, if their earnings are less than 50% of basic pay (guaranteed hourly rate), earning of the workers will be as follows: Workers A and C will be paid the wages as computed viz., Rs9,120 and Rs12,600 respectively. The computed earnings under piece rate basis for worker B is Rs3,000 which is less than 50% of basic pay i.e., Rs 4,400 (Rs8,800 × 50%) therefore B would be paid Rs6,600 i.e. 75% × Rs8,800 .

Working Notes:

(i) Piece rate / perunit

|

Product |

Standard time per unit in minutes |

Piece rate each minute (Rs) |

Piece rate per unit (Rs) |

|

(a) |

(b) |

(c) |

(d) = (b) × (c) |

|

P

Q

R |

12

18

30 |

1.00

1.00

1.00 |

12.00

18.00

30.00 |

(ii) Time allowed to each worker

Worker A = (84 units × 12 minutes) + (144 units × 18 minutes) + (184 units × 30 minutes)

= 9,120 minutes or 152 hours

Worker B = 100 units × 30 minutes

= 3,000 minutes or 50 hours

Worker C = (240 units × 12 minutes) + (540 units × 18 minutes)

= 12,600 minutes or 210 hours

Question 33

The existing incentive system of Alpha Limited is as under:

Normal working week 5 days of 8 hours each plus 3 late shifts of 3 hours each

Rate of Payment:

Day work: Rs160 per hour

Late shift: Rs225 per hour

Average output per operator for 49-hours 240 articles week i.e. including 3 late shifts

In order to increase output and eliminate overtime, it is decided to switch on to a system of payment by results. The following information is obtained:

Time-rate (as usual) :Rs160 per hour

Basic time allowed for 15 : 2.5 hours articles

Piece-work rate : Add 20% to basic piece rate

Premium Bonus : Add 50% to time.

If during the last week 270 articles are produced in a 40-hour week.

Required:

(i) CALCULATE weekly earnings, number of articles produced and labour cost per article for one operator under the following systems:

(a) Existing time-rate

b)Straight piece-work

c) Rowan system

d) Halsey premium system

(ii) PREPARE a Statement showing hours worked, weekly earnings, number of articles produced and labour cost per article for one operator under the above systems.

Answer:

(i) (a) Existing time rate

Question 34

Discuss the treatment of under-absorbed and over-absorbed factory overheads in cost accounting.

Answer

Treatment of under absorbed and over absorbed factory overheads in cost accounting: Factory overheads are usually applied to production on the basis of pre-determined rate

= Estimated normal overheads for the period / Budgeted No. of units during the period

The possible options for treating under / over absorbed overheads are

-

Use supplementary rate in the case of substantial amount of under / over absorption

-

Write it off to the costing profit & loss account in the event of insignificant amount / or abnormal reasons.

-

Carry forward to next accounting period if operating cycle exceeds one year.

Question 35

Discuss the step method and reciprocal service method of secondary distribution of overheads.

Answer

Step method and Reciprocal Service method of secondary distribution of overheads

Step method: This method gives cognisance to the service rendered by service department to another service dep’t, thus sequence of apportionments has to be selected. The sequence here begins with the dep’t that renders service to the max number of other service dep’t. After this, the cost of service dep’t serving the next largest number of dep’t is apportioned.

Reciprocal service method : This method recognises the fact that where there are two or more service dep’t, they may render service to each other and, therefore, these inter dep’t services are to be given due weight while re-distributing the expense of service dep’t. The methods available for dealing with reciprocal servicing are:

-

Simultaneous equation method

-

Repeated distribution method

-

Trial and error method.

Question 36

Explain: Single and multiple overhead rate.

Answer

Single and multiple overhead rate: A single overhead rate, when computed for the entire factory is known as the blanket rate.

Blanket rate = Overhead cost of entire factory / total quantum of the base selected

The blanket rates can be utilised in the following cases;

i) Where only one major product is being produced.

ii)Where several products are produced but: (a) all products pass through all departments and (b) all products require the same length of time in each department.

When the above conditions are not applicable, separate departmental rates should be used. Multiple rates involve computation of separate rates for each production department, service department, cost-centre, each product or line and each production factor.

Question 37

Discuss the treatment of research and development expenditures in cost accounting.

Answer

If research is conducted in the methods of production, the expenses should be charged to production overhead. If the research relates to administration, the expenses are charged to administration overheads. If it is related to market research, the expenses are charged to S&D overheads. Development costs incurred in connection with a particular product should be charged directly to that product. Such expenses are usually treated as deferred revenue expenditure and recovered as cost per unit of the product when production is fully established. Routine nature research expenses are charged to general overheads.

Question 38

A manufacturing unit has purchased and installed a new machine of Rs12,70,000to its fleet of 7 existing machines. The new machine has an estimated life of 12 years and is expected to realise Rs70,000 as scarp at the end of its working life. Other relevant data are as follows:

-

Budgeted working hours are 2,592 based on 8 hours per day for 324 days. This includes 300hoursforplantmaintenanceand92hoursforsettingupofplant.

-

Estimated cost of maintenance of the machine is Rs25,000(p.a.).

-

Rs The machine requires a special chemical solution, which is replaced at the end of each week (6 days in a week) at a cost of Rs400 each time.

-

Four operators control operation of 8 machines and the average wages per person amounts to Rs420 per week plus 15% fringe benefits.

-

Electricity used by the machine during the production is 16 units per hour at a cost of Rs3 per unit. No current is taken during maintenance and setting up.

-

Departmental and general works overhead allocated to the operation during last year was Rs50,000. During the current year it is estimated to increase 10% of this amount.

Calculate machine hour rate, if (a) setting up time is unproductive; (b) setting up time is productive.

Answer

Computation of Machine hour Rate

|

|

Per year |

Per hour (unproductive) |

Per hour (productive) |

|

Standing charges |

|

|

|

|

Operators wages |

|

|

|

|

4 × 420 × 54 |

90,720 |

|

|

|

Add: Fringe Benefits 15% |

13,608 |

|

|

|

|

1,04,328 |

|

|

|

Departmental and general overhead |

|

|

|

|

(50,000 + 5,000) |

55,000 |

|

|

|

Total Std. Charging for 8 machines |

1,59,328 |

|

|

|

Cost per Machine 1,59,328/8 |

19,916 |

|

|

|

Cost per Machine hour 19,916/2,200 |

|

9.05 |

|

|

19,916/2,292 |

|

|

8.69 |

|

Machine hours: |

|

|

|

|

Setting time unproductive (2,592-300-92)= 2200 |

|

|

|

|

Setting time productive (2,592-300) = 2,292 |

|

|

|

|

Machine expenses |

|

|

|

|

Depreciation (12,70,000 -70,000)/(12 × 2,200) |

|

45.45 |

|

|

(12,70,000-70,000)/(12 × 2,292) |

|

|

43.63 |

|

Electricity (16 × 3) |

|

48.00 |

|

|

(16 × 3 × 2,200)/2,292) |

|

|

46.07 |

|

Special chemical solution (400 × 54)/2,200/ 2,292 |

|

9.82 |

9.42 |

|

Maintenance (25,000/2,200) |

|

11.36 |

|

|

(25,000/2,292) |

|

|

10.91 |

|

Machine Hour Rate |

|

123.68 |

118.72 |

Question 39

From the details furnished below you are required to compute a comprehensive machine-hour rate:

|

Original purchase price of the machine (subject to depreciation at 10% per annum on original cost) |

|

Rs3,24,000 |

||||||||

|

Normal working hours for the month |

|

200 hours |

||||||||

|

(The machine works to only 75% of capacity) |

|

|

||||||||

|

Wages of Machine man |

Rs125 per day (of 8 hours) |

|

||||||||

|

Wages for Helper (machine attendant) |

Rs75 per day (of 8 hours) |

|

||||||||

|

Power cost for the month for the time worked |

|

Rs 15,000 |

||||||||

|

Supervision charges apportioned for the machine centre for the month |

|

Rs 3,000 |

||||||||

|

Electricity & Lighting for the month |

|

Rs 7,500 |

|

Repairs & maintenance (machine) including Consumable stores per month |

|

|

|

Consumable stores per month |

|

Rs 17,500 |

|

Insurance of Plant & Building (apportioned) for the year |

|

Rs 16,250 |

|

Other general expense per annum |

|

Rs 27,500 |

The workers are paid a fixed Dearness allowance of Rs1,575 per month. Production bonus payable to workers in terms of an award is equal to 33.33% of basic wages and dearness allowance. Add 10% of the basic wage and dearness allowance against leave wages and holidays with pay to arrive at a comprehensive labour-wage for debit to production.

Answer

Computation of Comprehensive Machine Hour Rate

|

|

Per month(Rs) |

Per hour(Rs) |

|

Fixed cost |

|

|

|

Supervision charges |

3,000 |

|

|

Electricity and lighting |

7,500 |

|

|

Insurance of Plant and building |

1,354.17 |

|

|

(16,250×1/12) |

|

|

|

Other General Expenses (27,500×1/12) |

2,291.67 |

|

|

Depreciation (32,400×1/12) |

2,700 |

|

|

|

16,845.84 |

112.31 |

|

Variable Cost |

|

|

|

Repairs and maintenance |

17,500 |

116.67 |

|

Power |

15,000 |

100.00 |

|

Wages of machine man |

|

44.91 |

|

Wages of Helper |

|

32.97 |

|

Machine Hour rate (Comprehensive) |

|

Rs 406.86 |

Effective machine working hour’s p.m.

200 hrs. × 75% = 150 hrs.

Wages per machine hour

|

|

Machine man |

Helper |

|

Wages for 200 hours |

|

|

|

(Rs 125× 25) |

Rs 3,125 |

|

|

(Rs 75× 25) |

|

Rs 1,875 |

|

D.A. |

Rs 1,575 |

Rs 1,575 |

|

|

Rs 4,700 |

Rs 3,450 |

|

Production bonus (1/3 of above) |

1,567 |

1,150 |

|

|

6,267 |

4,600 |

|

Leave wages (10%) |

470 |

345 |

|

|

6,737 |

4,945 |

|

Effective wage rate per machine hour (150 hrs in all) |

Rs44.91 |

Rs32.97 |

Question 40

Discuss the accounting of Selling and Distribution overheads.

Answer

Accounting of Selling and Distribution Overheads

It is difficult to determine an entirely satisfactory basis for computing the overhead rate for absorbing selling and distribution overheads. The basis usually adopted is:

-

Sales value of goods

-

Cost of goods sold

-

Gross profit on sales

-

Number of orders or units sold

|

Expenses |

Basis for allocation |

|

Salaries in Sales Department Advertisements Show room expenses Rent of finished goods, go downs and expenses on own delivery vans. |

Estimated time devoted to the sale of various products. Actual amount incurred for each product Average space occupied by each product Average quantities delivered during a period |

Question 41

RST Ltd. has two production departments: Machining and Finishing. There are three service departments: Human Resource (HR), Maintenance and Design. The budgeted costs in these service departments are as follows:

|

|

HR Rs |

Maintenance Rs |

Design Rs |

|

Variable |

1,00,000 |

1,60,000 |

1,00,000 |

|

Fixed |

4,00,000 |

3,00,000 |

6,00,000 |

|

|

5,00,000 |

4,60,000 |

7,00,000 |

The usage of these Service Departments’ output during the year just completed is as follows: Provision of Service Output (in hours of service)

|

Users of Service |

Providers of Service |

||||

|

HR |

Maintenance |

Design |

|||

|

HR |

|

|

|

||

|

Maintenance |

500 |

|

|

||

|

Design |

500 |

500 |

|

||

|

Machining |

4,000 |

3,500 |

4,500 |

||

|

Finishing |

5,000 |

4,000 |

1,500 |

|

Total |

10,000 |

8,000 |

6,000 |

Required:

(i) Use the direct method to re-apportion RST Ltd.’s service department cost to its production departments.

(ii) Determine the proper sequence to use in re-apportioning the firm’s service department cost by step-down method.

(iii) Use the step-down method to reapportion the firm’s service department cost.

Answer

(i) Apportionment of Service Department Overheads amongst production departments using Direct Method:

|

|

Production Deptts. |

Service Deptts. |

|||

|

Machining Rs |

Finishing Rs |

HR Rs |

Maintenance Rs |

Design Rs |

|

|

Overhead as per primary distribution |

|

|

5,00,000 |

4,60,000 |

7,00,000 |

|

Apportionment design |

5,25,000 |

1,75,000 |

|

|

|

|

4,500 : 1,500 |

|

|

|

|

|

|

Maintenance |

2,14,667 |

2,45,333 |

|

|

|

|

3,500 : 4,000 |

|

|

|

|

|

|

HR 4,000 : 5,000 |

2,22,222 |

2,77,778 |

|

|

|

|

|

9,61,889 |

6,98,111 |

|

|

|

(ii) The proper sequence for apportionment of service department overheads is

First HR

Second Maintenance

Third Design

The sequence has been laid down based on service provided.

(iii) Apportionment of Service Department overheads amongst production departments using step-down method.

|

|

Production Department |

Service Department |

|||

|

Machining Rs |

Finishing Rs |

HR Rs |

Maintenance Rs |

Design Rs |

|

|

Overhead as per |

|

|

5,00,000 |

4,60,000 |

7,00,000 |

|

primary |

|

|

( )5,00,000 |

25,000 |

|

|

distribution |

2,00,000 |

2,50,000 |

|

( )4,85,000 |

25,000 |

|

Apportionment HRD 4 |

|

|

|

|

|

|

: 5 : : 0.5 : 0.5 |

2,12,188 |

2,42,500 |

|

|

30,312 |

|

Maintenance 7 : 8: : 1 |

5,66,484 |

1,88,828 |

|

|

( )7,55,312 |

|

Design 3 : 1 |

9,78,672 |

6,81,328 |

|

|

|

Question 42

Explain briefly the conditions when supplementary rates are used.

Answer

When the amount of under absorbed and over absorbed overhead is significant or large, because of differences due to wrong estimation, then the cost of product needs to be adjusted by using supplementary rates (under and over absorption/actual overhead) to avoid misleading impression.

Question 43

Distinguish between Fixed overheads and Variable overheads.

Answer

Fixed overheads v/s Variable Overheads

Fixed overheads are not affected by any variation in the volume of activity, e.g., managerial remuneration, rent etc. These remain the same from one period to another except when they are deliberately changed.Fixed overheads are generally variable per unit of output or activity.

On other hand the variable overheads that change in proportion to the change in the volume of activity or output, e.g., power consumed, consumable stores etc. The variable overheads are generally constant per unit of output or activity

Question 44

What are the methods of re-apportionment of service department expenses over the production departments? Discuss.

Answer

Methods of re-apportionment of service department expenses over the production departments

-

Direct re-distribution method.

-

Step method or non-reciprocal method.

-

Reciprocal Service method

Direct re-distribution Method: Service department costs under this method are apportioned over the production departments only, ignoring services rendered by one service department to another.The basis of apportionment could be no. of workers .H.P of machines.

Step Method or Non-Reciprocal Method:

This method gives cognizance to the service rendered by service department to another service department. Therefore, as compared to previous method, this method is more complicated because a sequence of apportionments has to be selected here. The sequence here begins with the department that renders service to the maximum number of other service departments.

|

Production Department |

Service Department |

||||

|

P1

|

P

|

P3

|

S1

|

S2

|

S3

|

|

|

|

|

|

|

|

Reciprocal Service Method:

This method recognizes the fact that where there are two or more service departments they may render service to each other and, there these inter-departmental services are to be given due weight while re-distributing the expenses of service department.

The methods available for dealing with reciprocal services are:

-

Simultaneous equation method

-

Repeated distribution method

-

Trial &Error method.

Question 45

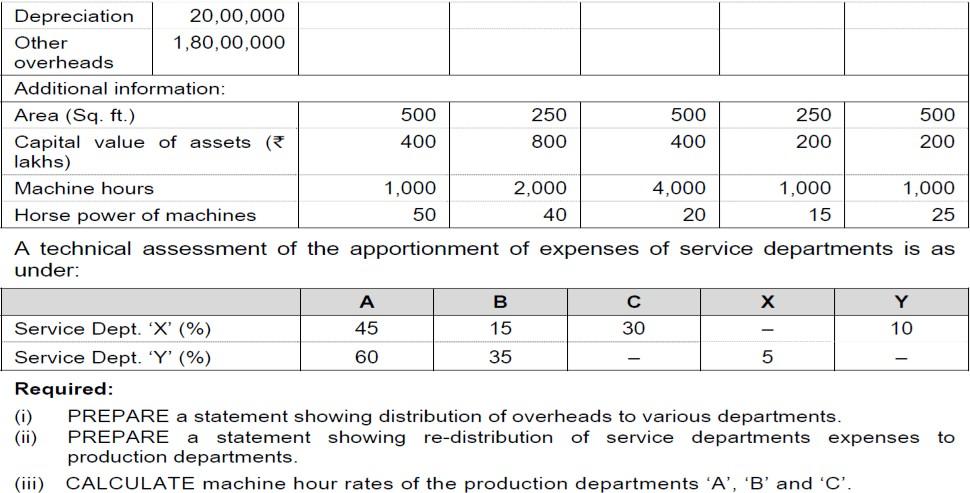

You are given the following information of the three machines of a manufacturing department of X Ltd.:

|

|

Preliminary estimates of expenses (per annum) |

|||

|

Total (Rs) |

Machines |

|||

|

A (Rs) |

B (Rs) |

C (Rs) |

||

|

Depreciation |

20,000 |

7,500 |

7,500 |

5,000 |

|

Spare parts |

10,000 |

4,000 |

4,000 |

2,000 |

|

Power |

40,000 |

|

|

|

|

Consumable stores |

8,000 |

3,000 |

2,500 |

2,500 |

|

Insurance of machinery |

8,000 |

|

|

|

|

Indirect labour |

20,000 |

|

|

|

|

Building maintenance expenses |

20,000 |

|

|

|

|

Annual interest on capital outlay |

50,000 |

20,000 |

20,000 |

10,000 |

|

Monthly charge for rent and rates |

10,000 |

|

|

|

|

Salary of foreman (per month) |

20,000 |

|

|

|

|

Salary of Attendant (per month) |

5,000 |

|

|

|

(The foreman and the attendant control all the three machines and spend equal time on them) The following additional information is also available:

|

|

Machines |

||

|

A |

B |

C |

|

|

Estimated Direct Labour Hours |

1,00,000 |

1,50,000 |

1,50,000 |

|

Ratio of K.W. Rating |

3 |

2 |

3 |

|

Floor space (sq. ft.) |

40,000 |

40,000 |

20,000 |

There are 12 holidays besides Sundays in the year, of which two were on Saturdays. The manufacturing department works 8 hours in a day but Saturdays are half days. All machines work at 90% capacity throughout the year and 2% is reasonable for breakdown.

You are required to :

Calculate predetermined machine hour rates for the above machines after taking into consideration the following factors:

-

An increase of 15% in the price of spare parts.

-

Anincreaseof25%intheconsumptionofsparepartsformachine‘B’&‘C’only. 20% general increase in wages rates.

Answer

Computation of Machine Hour Rate

|

|

Basis of apportionment |

Total |

Machines |

||

|

A |

B |

C |

|||

|

Rs |

Rs |

Rs |

Rs |

||

|

(A) Standing Charges |

|

|

|

|

|

|

Insurance |

Depreciation Basis |

8,000 |

3,000 |

3,000 |

2,000 |

|

Indirect Labour |

Direct Labour |

24,000 |

6,000 |

9,000 |

9,000 |

|

Building Maintenance expenses |

Floor Space |

20,000 |

8,000 |

8,000 |

4,000 |

|

Rent and Rates |

Floor Space |

1,20,000 |

48,000 |

48,000 |

24,000 |

|

Salary of foreman |

Equal |

2,40,000 |

80,000 |

80,000 |

80,000 |

|

Salary of attendant |

Equal |

60,000 |

20,000 |

20,000 |

20,000 |

|

Total standing charges |

|

4,72,000 |

1,65,000 |

1,68,000 |

1,39,000 |

|

Hourly rate for standing charges |

|

|

84.75 |

86.29 |

71.40 |

|

(B) Machine Expenses: |

|

|

|

|

|

|

Depreciation |

Direct |

20,000 |

7,500 |

7,500 |

5,000 |

|

Spare parts |

Final estimates |

13,225 |

4,600 |

5,750 |

2,875 |

|

Power |

K.W. rating |

40,000 |

15,000 |

10,000 |

15,000 |

|

Consumable Stores |

Direct |

8,000 |

3,000 |

2,500 |

2,500 |

|

Total Machine expenses |

|

81,225 |

30,100 |

25,750 |

25,375 |

|

Hourly Rate for Machine expenses |

|

|

15.46 |

13.23 |

13.03 |

|

Total (A + B) |

|

553,225 |

1,95,100 |

1,93,750 |

1,64,375 |

|

Machine Hour rate |

|

|

100.21 |

99.52 |

84.43 |

Working Notes:

(i) Calculation of effective working hours:

No. of holidays 52 (Sundays) + 12 (other holidays) = 64 Saturday (52 – 2) = 50

No. of days (Work full time) = 365 – 64 – 50 = 251

(iii) Amount of Indirect Labour is calculated as under:

|

|

Rs |

|

Preliminary estimates |

20,000 |

|

Add: Increase in wages @ 20% |

4,000 |

|

|

24,000 |

-

Interest on capital outlay is a financial matter and, therefore it has been excluded from the cost accounts.

Question 46

How do you deal with the following in cost account?

-

Packing Expenses

-

Fringe benefits Answer

Packing expenses: Cost of primary packing necessary for protecting the product or for convenient handling, should become a part of the prime cost. The cost of packing to facilitate the transportation of the product from the factory to the customer should become a part of the distribution cost. If the cost of special packing is at the request of the customer, the same should be charged to the specific work order or the job. The cost of fancy packing necessary to attract customers is an advertising expenditure. Hence, it is to be treated as a selling overhead.

Fringe benefits: These are the additional payments or facilities provided to the workers apart from their salary and direct cost-allowances like house rent and city compensatory allowances. If the amount of fringe benefit is considerably large, it may be recovered as direct charge by means of a supplementary wage or labour rate; otherwise these may be collected as part of production overheads.

Question 47

The following account balances and distribution of indirect charges are taken from the accounts of a manufacturing concern for the .year ending on 31st March,2012:

|

Item |

Total Amount |

Production Departments |

Service Departments |

|||

|

(Rs) |

X (Rs) |

Y (Rs) |

Z (Rs) |

A (Rs) |

B (Rs) |

|

|

Indirect Material |

1,25,000 |

20,000 |

30,000 |

45,000 |

25,000 |

5,000 |

|

Indirect Labour |

2,60,000 |

45,000 |

50,000 |

70,000 |

60,000 |

35,000 |

|

Superintendent's Salary |

96,000 |

- |

- |

96,000 |

- |

- |

|

Fuel & Heat |

15,000 |

|

|

|

|

|

|

Power |

1,80,000 |

|

|

|

|

|

|

Rent & Rates |

1,50,000 |

|

|

|

|

|

|

Insurance |

18,000 |

|

|

|

|

|

|

Meal Charges |

60,000 |

|

|

|

|

|

|

Depreciation |

2,70,000 |

|

|

|

|

|

The following departmental data are also available:

|

|

Production Departments |

Service Departments |

|||

|

X |

Y |

Z |

A |

B |

|

|

Area (Sq. ft.) |

4,400 |

4,000 |

3,000 |

2,400 |

1,200 |

|

Capital Value of Assets (Rs) |

4,00,000 |

6,00,000 |

5,00,000 |

1,00,000 |

2,00,000 |

|

Kilowatt Hours |

3,500 |

4,000 |

3,000 |

1,500 |

- |

|

Radiator Sections |

20 |

40 |

60 |

50 |

30 |

|

No. of Employees |

60 |

70 |

120 |

30 |

20 |

Expenses charged to the service departments are to be distributed to other departments by the following percentages:

|

|

X |

Y |

Z |

A |

B |

|

Department A Department B |

30 25 |

30 40 |

20 25 |

- 10 |

20 - |

Prepare an overhead distribution statement to show the total overheads of production departments after re-apportioning service departments' overhead by using simultaneous equation method.' Show all the calculations to the nearestrupee.

Answer

Primary Distribution of Overheads

|

Item |

Basis |

Total Amount (Rs) |

Production Departments |

Service Departments |

|||

|

X (Rs) |

Y (Rs) |

Z (Rs) |

A (Rs) |

B (Rs) |

|||

|

Indirect Material |

Actual |

1,25,000 |

20,000 |

30,000 |

45,000 |

25,000 |

5,000 |

|

Indirect Labour |

Actual |

2,60,000 |

45,000 |

50,000 |

70,000 |

60,000 |

35,000 |

|

Superintendent’s Salary |

Actual |

96,000 |

- |

- |

96,000 |

- |

- |

|

Fuel & Heat |

Radiator Sections {2:4:6:5:3} |

15,000 |

1,500 |

3,000 |

4,500 |

3,750 |

2,250 |

|

Power |

Kilowatt Hours {7:8:6:3:0} |

1,80,000 |

52,500 |

60,000 |

45,000 |

22,500 |

- |

|

Rent & Rates |

Area (Sq. ft.) {22:20:15:12:6} |

1,50,000 |

44,000 |

40,000 |

30,000 |

24,000 |

12,000 |

|

Insurance |

Capital Value of Assets {4:6:5:1:2} |

18,000 |

4,000 |

6,000 |

5,000 |

1,000 |

2,000 |

|

Meal Charges |

No.of Employees {6:7:12:3:2} |

60,000 |

12,000 |

14,000 |

24,000 |

6,000 |

4,000 |

|

Depreciation |

Capital Value of Assets {4:6:5:1:2} |

2,70,000 |

60,000 |

90,000 |

75,000 |

15,000 |

30,000 |

|

Total overheads |

|

11,74,000 |

2,39,000 |

2,93,000 |

3,94,500 |

1,57,250 |

90,250 |

Secondary Distribution of Overheads

|

|

Production Departments |

||

|

X (Rs) |

Y (Rs) |

Z (Rs) |

|

|

Total overhead as per primary distribution |

2,39,000 |

2,93,000 |

3,94,500 |

|

Service Department A (80% of 1,69,668) |

50,900 |

50,900 |

33,934 |

|

Service Department B (90% of 1,24,184) |

31,046 |

49,674 |

31,046 |

|

Total |

3,20,946 |

3,93,574 |

4,59,480 |

Question 48

Distinguish between cost allocation and cost absorption.

Answer

Distinguish between Cost allocation and Cost absorption:

Cost allocation is the allotment of whole item of cost to a cost centre or a cost unit. In other words, it is the process of identifying, assigning or allowing cost to a cost centre or a cost unit.

Cost absorption is the process of absorbing all indirect costs or overhead costs allocated or apportioned over particular cost center or production department by the units produced.

Question 49

Explain the treatment of over and under absorption of overheads in cost accounts.

Answer

Treatment of over and under absorption of overheads are:-

-

Writing off to costing P&L A/c:– Small difference between the actual and absorbed amount should simply be transferred to costing P&L A/c, if difference is large then investigate the causes and after that abnormal loss/ gain shall be transferred to costing P&LA/c.

-

Use of supplementary Rate: Under this method the balance of under and over absorbed overheads may be charged to cost of W.I.P., finished stock and cost of sales proportionately with the help of supplementary rate ofoverhead.

-

Carry Forward to Subsequent Year: Difference should be carried forward in the expectation that next year the position will be automatically corrected.

Question 50

(Re-apportionment of overheads using Trial and Error Method):

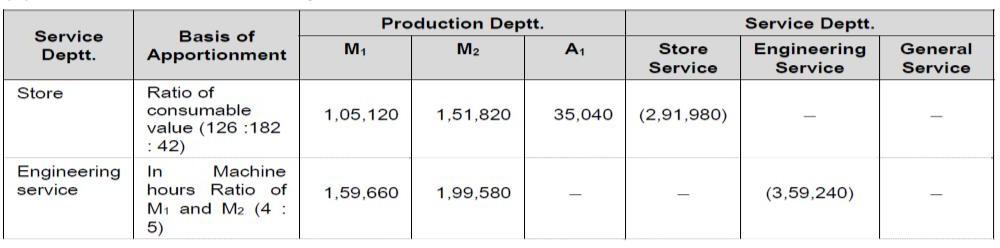

SA Ltd. has three production (M1, M2 and A1) and three service departments (Stores, Engineering services and General service). Engineering department serves the M1 and M2 only.

The relevant information related with Product X and Y are as follows:

(Rs)

-

Depreciation on Machinery 7,92,000

-

Insurance of Machinery 1,44,000

-

Insurance of Building 64,800 (Total building insurance cost for M1 is one third of annual premium)

-

Power 1,29,600

-

Light 1,08,000

-

Rent 2,53,500 (The general service deptt. is located in a building owned by the company. It is valued at Rs1,20,000 and is charged into cost at notional value of 8% per annum. This cost is additional to the rent shown above)

The value of issues of materials to the production departments are in the same proportion as shown above for the Consumable supplies.

The following data are also available:

Required:

(i) PREPARE an overhead analysis sheet, showing the bases of apportionment of overhead to departments.

(ii)PREPARE a statement allocating service department overheads to production department ignoring the apportionment of service department costs among service departments.

(iii) CALCULATE suitable overhead absorption rate for the production departments.

(iv) CALCULATE the overheads to be absorbed by two products, X and Y.

Answer:

(i) Summary of Apportionment of Overheads

(Rs)

*Rent to be apportioned among the departments which actually use the rented building. The notional rent is imputed cost and is not included in the calculation.

ii) Allocation of service departments overheads

Answer:

(i) Overhead Distribution Summary

Question 51

Why is it necessary to reconcile the Profits between the Cost Accounts and Financial Accounts?

Answer

When the cost and financial accounts are kept separately, it is imperative that these should be reconciled, otherwise the cost accounts would not be reliable. The reconciliation of two set of accounts can be made, if both the sets contain sufficient detail as would enable the causes of differences to be located. It is, therefore, important that in the financial accounts, the expenses should be analysed in the same way as in cost accounts. It is important to know the causes which generally give rise to differences in the costs & financial accounts. These are:

(i) Items included in financial accounts but not in cost accounts Appropriation of

-

profits Income-tax

-

Transfer to reserve

-

Dividends paid

-

Goodwill / preliminary expenses written off

-

Pure financial items

-

Interest, dividends

-

Losses on sale of investments

-

Expenses of Co’s share transfer office Damages & penalties

(ii) Items included in cost accounts, but not in financial accounts

-

Opportunity cost of capital

-

Notional rent

(iii)Under / Over absorption of expenses in cost accounts

(iv) Different bases of inventory valuation Motivation for reconciliation are:

-

To ensure reliability of cost data

-

To ensure ascertainment of correct product cost

-

To ensure correct decision making by the management based on cost & financial data

-

To report fruitful financial / cost data

Question 53

The following figures have been extracted from the cost records of a manufacturing unit:

|

|

Rs |

|

Stores: Opening balance |

32,000 |

|

Purchases of material |

1,58,000 |

|

Transfer from work-in-progress |

80,000 |

|

Issues to work-in-progress |

1,60,000 |

|

Issues to repair and maintenance |

20,000 |

|

Deficiencies found in stock taking |

6,000 |

|

Work-in-progress: Opening balance |

60,000 |

|

Direct wages applied |

65,000 |

|

Overheads applied |

2,40,000 |

|

Closing balance of W.I.P. |

45,000 |

Finish products: Entire output is sold at a profit of 10% on actual cost from work-in- progress. Wages incurred Rs70,000, overhead incurred Rs2,50,000.

Items not included in cost records: Income from investment Rs10,000, Loss on sale of capital assets Rs20,000.